What is a variable annuity and how do they work? If you are looking for an account that can pay you back in more ways than one, then this might be a good choice for you.

What is an annuity, or more specifically, what is a variable annuity, a fixed annuity, or a deferred annuity? All of these are types of annuity contracts.

An annuity is a type of account that manages funds and pays those funds to the account holder. Some people might use an annuity to hold their settlement money after a personal injury case. Some people might even use this type of account to hold their retirement funds, which will then be paid back to the account holder in retirement through regularly scheduled payments.

Basically, if you need to hold funds in a safe and secure place, and you also want to receive regular disbursements or payments from that account, then that's what an annuity account is for.

Variable annuity accounts can be used for many reasons like retirement funds, setting up a structured settlement, or to hold investment funds from an investment portfolio. They might be used to help manage mutual funds. This is an investment portfolio that provides multiple investment options.

Whether you are using this type of account for retirement, settlement money, or an investment portfolio, it is a good idea to understand the difference between the different kinds of annuity accounts. This will help you pick out the right kind of account for your specific needs.

There are essentially three parts to any annuity account: the principal amount that was initially deposited into the account, the rate that principal amount grows, and the scheduled disbursement payments to the account holder. These three parts can be separated into two phases: the accumulation phase and the payout phase.

The accumulation of funds into this account can sometimes be called the accumulation phase. This is the first phase of the variable annuity contract.

This first phase has to do with the principal amount of the account. The principal amount refers to the initial amount of money placed in the account. Accounts like these will require an initial deposit which will be the principal. You can purchase an annuity contract with one lump sum payment or with several payments.

For those who are in a personal injury lawsuit and looking to manage their settlement funds, their accumulation phase may consist of their lawyer organizing the deposit of settlement funds into an annuity.

The second phase of the contract is the beginning of the flow of income disbursements from the account. This phase can be called the payout phase or the distribution phase.

There are many ways to organize the payout phase. An annuity account holder can receive disbursements from this account in regularly scheduled payments (like once a month or once a year) or the funds can be made available after a certain amount of time.

This account could also grow according to the interest rate associated with the account, or by how well the investments tied to the account are doing. Depending on the growth characteristics of the account, you could choose to receive a fixed income or a variable income that is based on how well the investments linked to the account are doing.

A variable annuity was created after the fixed annuity to provide even more options for how to set up this type of account. Variable annuities come with more flexible payment amount options for the payout phase. With a variable annuity, payments have the potential to rise as the market rises or as certain investments do well.

The downside to this type of account is that if the market isn't doing well, then your payments in the payout phase will be lower. Because your payments are linked to the market, this account option becomes has more market risk, but with the potential to do really well if the market does perform well.

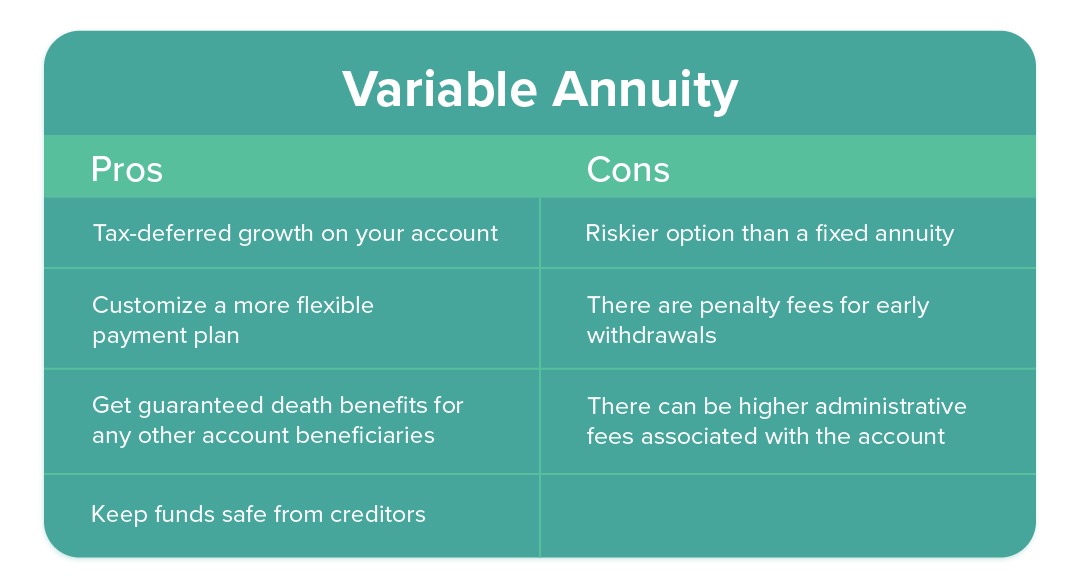

These accounts have many benefits to consider. For example, this account has tax-deferred growth, which means you won't need to pay taxes on these funds until after you start receiving the funds as income. That way your account funds can grow without being depleted at all by taxes.

Because these accounts are more flexible you can also customize the way you receive payments even more than you can with a fixed annuity. It may be the option with more market risk but with that market risk comes the potential for higher returns and bigger payouts.

You do need to be aware of the certain downsides you will have to accept by using a variable annuity. The risks involved can be really helpful, but they do come with a lack of security that you might enjoy with a fixed annuity.

A fixed annuity was the first kind of annuity account created. Fixed annuities come with a fixed payment amount for the payout phase. With a fixed annuity, payments have the security of staying the same no matter what happens in the market.

The downside to variable annuities is that if the market does really well, then your payments will still remain the same and not benefit from that rising market. But, because your payments are not linked to the market, this account option becomes the least risky choice.

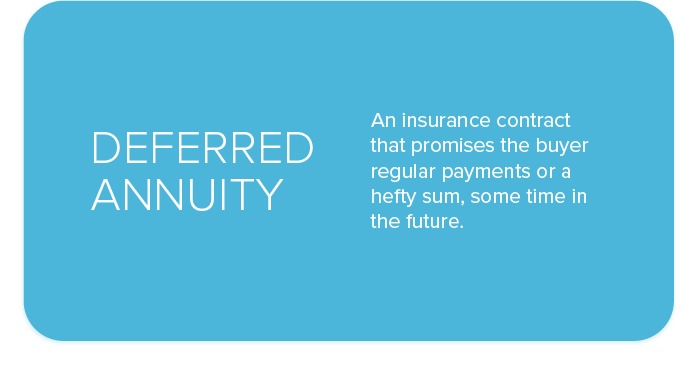

A deferred annuity was created to give account holders the option of receiving payments at a later, future date. With this feature, you can set up future payments for retirement for example. Having a retirement plan and a retirement account like an IRA or 401K is a good idea, but having an extra account like this can give you even more security in your retirement days.

A variable annuity is a perfect way to help add to your retirement plans because it is also structured to give you regular payments at some point, just like income.

This type of account is the opposite of an immediate annuity, which starts the payout phase immediately rather than at a future date. An immediate annuity might be more commonly used

Whether you are looking for a way to organize a life insurance policy, investment options, mutual funds, retirement plans, or settlement funds, an annuity can be a great way to increase your financial portfolio. You can even consult with a financial professional to help you go over your options.